Investors are currently considering whether the US equity market is experiencing a bubble relating to Artificial Intelligence (AI). This article briefly explores this issue.

What is a financial bubble? A bubble is an unsustainable surge in the price of assets, where valuations far exceed the assets’ underlying fundamental worth. Bubbles can be driven by factors such as material technology change or low interest rates. They are difficult to identify in real-time and are usually only confirmed after they burst.

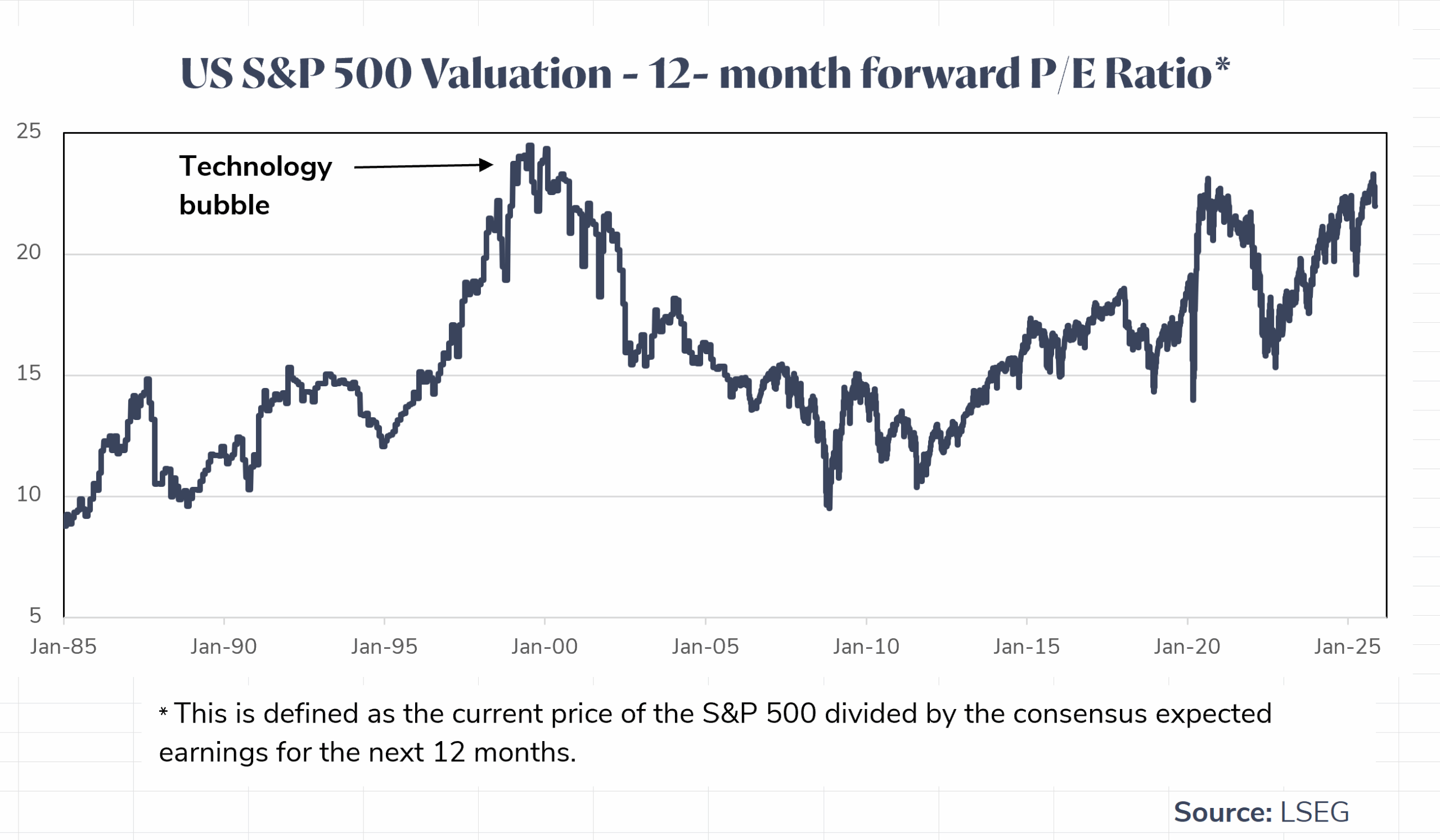

Recent examples of financial bubbles include the US technology bubble (1997 to 2000) and the US housing bubble (2004 to 2006). Following both bubbles, there was a material correction in the US equity market.

There are some signs that an AI bubble is currently occurring. For example, the forward price to earnings ratio of the S&P 500 is close to the peak level during the technology bubble (see chart below). This ratio is a commonly used valuation of the US equity market. Its current level is consistent with investors pricing much higher profit growth over the medium term than typically occurs. It is possible that the current pricing is reasonable. This could be the case if AI results in US productivity growth far exceeding its average level over recent decades.

Over recent months, investors have begun making comparisons between the current period and the technology bubble. For example, material technology change was a major driver of the US equity market during the technology bubble and that is also the case today. Another similarity is very rapid investment in the new technology. In the technology bubble, it was the fibre optic cables that underpinned the internet. Today it is the large language models and data centres that underpin AI tools.

While there are some similarities between the current environment and the technology bubble period, there are differences. One is that deterioration in US corporate balance sheets is so far less evident than was the case during the latter phase of the technology bubble. Also, the US Federal Reserve is currently cutting interest rates, which was not the case until after the technology bubble burst. These differences may mean that, even if a bubble is occurring, it may have further to run before an equity market correction occurs.

While we can’t be certain, our current assessment is that the US equity market is most likely experiencing a bubble phase. At this stage, we do not have a high level of conviction that a peak in the market is imminent but continue to monitor for signs of that occurring.

Investment returns are not guaranteed. Past performance is not a reliable indicator of future returns.

Issued by Vision Super Pty Ltd ABN 50 082 924 561 AFSL 225054. This information is general advice which does not take into account your personal financial objectives, situation or needs. Before making a decision about Vision Super, you should think about your financial requirements and consider the relevant Product Disclosure Statement and Target Market Determination